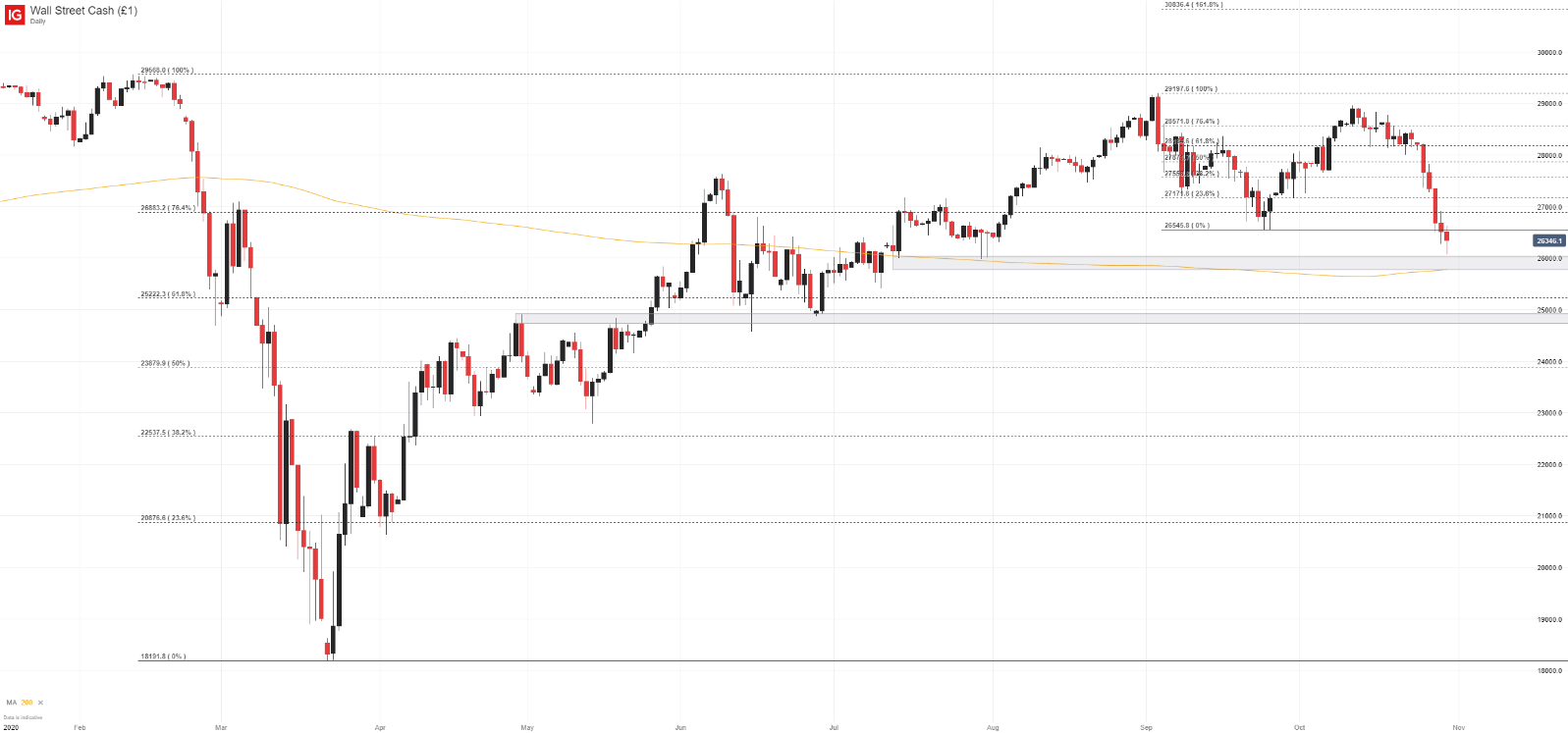

Wall Street is bracing for a cautious start as the Dow Jones Industrial Average points to a lower open. With a packed economic calendar and high-stakes corporate earnings on deck, investors are pulling back, favoring risk management over aggressive positioning. The slight premarket dip reflects broader unease—rising bond yields, persistent inflation signals, and a hawkish Federal Reserve tilt are all weighing on sentiment. This isn’t just another volatile week; it’s a potential pivot point for market direction in the months ahead.

Why the Dow Is Slipping at the Open

Pre-market movements often serve as a sentiment barometer, and today’s red ink in Dow futures signals investor hesitation. As of 6:30 AM ET, the Dow was down roughly 120 points, with the S&P 500 and Nasdaq also in negative territory. The sell-off isn’t driven by a single catalyst but rather a confluence of macro pressures:

- Rising Treasury Yields: The 10-year yield has climbed back above 4.6%, increasing pressure on equity valuations—particularly in rate-sensitive sectors like tech and real estate.

- Inflation Anxiety: Core CPI and PPI reports are due midweek, and expectations are for stubbornly elevated readings. Markets fear the Fed may have to hold rates higher for longer.

- Global Growth Concerns: Weak industrial data from China and Europe has fueled doubts about global demand, indirectly affecting multinational giants in the Dow.

Corporate headwinds also play a role. Procter & Gamble, a Dow component, reported mixed results yesterday, citing softer consumer spending. That news rippled through packaged goods and retail names, adding to the early-week caution.

Inflation Data in Focus: CPI, PPI, and Market Reaction

This week’s centerpiece is Wednesday’s Consumer Price Index (CPI) report. Economists project a 0.3% monthly increase in core CPI—up from 0.2% the prior month. Even a small beat could spark renewed volatility.

Historically, CPI releases have triggered immediate market reactions. For example:

- In June 2022, when CPI surged 9.1% year-over-year, the S&P 500 dropped 3% the next day.

- In July 2023, a cooler-than-expected print sparked a rally that pushed the Nasdaq up 4% over two sessions.

Investors aren’t just watching the headline number. Key components like shelter costs and services inflation will shape expectations for the Fed’s next move. If inflation proves sticky, bond yields could climb further, pressuring equities.

Producer Price Index (PPI) data, released a day later, offers a precursor to consumer prices. A hot PPI could confirm inflationary momentum, tightening the squeeze on markets ahead of Friday’s retail sales report.

Fed Voices: What Officials Are Saying

With CPI looming, every word from Federal Reserve officials carries extra weight. Last week, Fed Chair Jerome Powell reiterated that “policy rates may need to stay restrictive for some time.” He stopped short of committing to another hike but emphasized data dependence.

This week, speeches from several regional Fed presidents—Mary Daly, Thomas Barkin, and Michelle Bowman—are scheduled. Markets will parse their comments for clues on:

- Whether the Fed still sees upside inflation risks

- The timeline for potential rate cuts

- The central bank’s tolerance for prolonged tight policy

A dovish tone could spark a relief rally. But even a neutral message in this environment may be interpreted as hawkish, given elevated rate levels.

Traders are currently pricing in only a 30% chance of a rate hike at the July meeting. However, if inflation data surprises to the upside, those odds could shift rapidly—reshaping the entire interest rate outlook.

Earnings Season Kicks Into High Gear

While macro data dominates headlines, earnings are quietly driving stock-specific moves. This week brings reports from several Dow and S&P 500 heavyweights:

- Morgan Stanley (Tuesday): Eyes on trading revenue and wealth management flows. Net interest margin trends will also be key.

- Netflix (Tuesday): Subscribers growth in international markets could influence broader tech sentiment.

- Johnson & Johnson (Wednesday): As a defensive play, its guidance may reflect consumer health trends.

- Tesla (Wednesday): Deliveries and margin pressures remain top concerns. Any update on AI or robotics could sway sentiment.

- American Express (Thursday): A barometer for consumer spending, especially among higher-income groups.

Earnings aren’t just about numbers—they’re about narrative. A company beating estimates but issuing soft guidance can still see its stock drop. Conversely, managed downside surprises with optimistic outlooks sometimes spark rallies. This week, with macro uncertainty high, earnings resilience could become a differentiator.

Sector Watch: Where Investors Are Hiding

In uncertain markets, sector rotation intensifies. Right now, defensive plays are gaining traction:

- Utilities and Consumer Staples: These low-beta sectors are seeing inflows as investors seek stability.

- Healthcare: Johnson & Johnson and Merck provide ballast during volatility.

- Energy: Mixed signals. Oil prices are holding near $80, but demand concerns from Asia are a drag.

Meanwhile, rate-sensitive sectors are under pressure:

- Technology: Higher yields reduce the present value of future earnings, weighing on growth stocks.

- Real Estate: Rising mortgage rates are cooling housing activity. REITs have underperformed year-to-date.

- Financials: While higher rates boost net interest income, concerns about loan defaults in a slowing economy are growing.

The Dow’s composition—weighted toward industrials, healthcare, and financials—makes it particularly sensitive to shifts in economic growth expectations. A weaker-than-expected retail sales report Friday could trigger a broader sell-off.

Global Markets Add Pressure

U.S. markets don’t trade in a vacuum. Overseas, signs of stress are emerging:

- China: Industrial production and retail sales data released over the weekend came in below forecasts. Policy stimulus has been modest, fueling concerns about a sluggish recovery.

- Europe: The ECB hiked rates last week and signaled more tightening, despite weak growth. German bond yields are climbing, echoing U.S. trends.

- Japan: The yen continues to weaken past 150 per dollar, raising intervention fears. Any sudden move could ripple through currency and equity markets.

For multinational Dow components like Coca-Cola, Boeing, and Intel, soft overseas demand translates directly into lower revenue projections. Currency fluctuations also impact profit margins, adding another layer of complexity for investors.

Historical Context: What Past Data Weeks Tell Us

Looking back, weeks packed with CPI, Fed speeches, and major earnings often produce outsized moves:

- March 2023: Silicon Valley Bank collapse overshadowed CPI, but markets rallied on Fed liquidity measures.

- November 2022: A cooler CPI report sparked a relief rally—the S&P gained 5.4% that week.

- August 2021: Mixed data led to choppy trading, but tech stocks held up, driving Nasdaq gains.

The pattern? When data contradicts consensus, markets react sharply. But when expectations are aligned—like today’s cautious stance—volatility tends to be more contained unless a major surprise hits.

This week’s environment favors nimbleness. Investors who positioned early for a “higher for longer” rate scenario are better insulated. Those chasing momentum in tech or crypto may face tougher decisions.

Investor Strategy: Navigating the Noise

With so many catalysts in play, emotional discipline matters. Here’s a practical playbook for this week:

1. Avoid Front-Running CPI Many traders try to guess CPI outcomes and position early. More often than not, they get whipsawed. Instead, wait for the data, assess bond and futures reaction, then act.

2. Focus on Relative Strength Look for stocks outperforming during down markets. A company holding steady amid Dow weakness may be fundamentally strong.

3. Trim Overexposed Positions If you’re heavily weighted in rate-sensitive sectors, consider lightening up or using hedges like put options or inverse ETFs.

4. Watch Bond Markets Equities often follow Treasuries. A sudden yield spike on CPI day is a sell signal for many quantitative strategies.

5. Keep Cash Ready Volatility creates opportunity. Having dry powder lets you buy quality assets if markets overreact.

The Week Ahead: A Make-or-Break for Market Momentum

The Dow’s lower open sets the tone for a high-stakes week. Inflation data, Fed commentary, and corporate earnings will collectively answer a critical question: Is the market’s 2023 rally sustainable, or is it due for a correction?

There’s no single trade that wins in this environment. Success comes from preparation—knowing your entry and exit points, understanding macro linkages, and resisting the urge to overreact to hourly swings.

For long-term investors, this volatility is noise. For active traders, it’s opportunity. Either way, the next five days could define the market’s path for the rest of the year.

Stay informed, stay diversified, and don’t let headlines dictate decisions. The data will tell the real story—let it guide you.

FAQ

What should you look for in Dow Set to Open Lower Amid Key Economic Data Week? Focus on relevance, practical value, and how well the solution matches real user intent.

Is Dow Set to Open Lower Amid Key Economic Data Week suitable for beginners? That depends on the workflow, but a clear step-by-step approach usually makes it easier to start.

How do you compare options around Dow Set to Open Lower Amid Key Economic Data Week? Compare features, trust signals, limitations, pricing, and ease of implementation.

What mistakes should you avoid? Avoid generic choices, weak validation, and decisions based only on marketing claims.

What is the next best step? Shortlist the most relevant options, validate them quickly, and refine from real-world results.